In the world of personal finance, few topics have as many misconceptions as a credit score. It’s a three-digit number that can either open doors to financial opportunities or slam them shut. To put it simply – your credit score matters. From the belief that “checking your credit score will lower it” to “you only have one credit score,” myths can run wild when it comes to your credit score.

Here are seven of the most common credit score myths and the truth behind the crucial financial figure.

Myth: You only have one credit score.

Your credit score is the number that represents your creditworthiness. While it’s referred as your (singular) credit score, in reality, each person has multiple credit scores. This is because there are several consumer reporting agencies, and each one calculates scores differently. The three major credit bureaus in the United States are Experian, Equifax and TransUnion.

Each lender decides which credit bureau and which scoring model they want to use when they check your credit. The most well-known scoring models are FICO and VantageScore, but there are several others. This means you could potentially have dozens of credit scores. If you manage your credit responsibly, all your scores should be roughly in the same range.

Myth: Credit only matters when you need to borrow money.

It’s true that your credit score is a critical factor when lenders are determining whether to approve you for a loan or credit but that’s not all it’s used for. Your credit score can also affect other parts of your life.

Many landlords check credit scores when deciding whether to rent to someone. Some employers do credit checks as part of the hiring process, especially for jobs that involve handling money. Insurance companies sometimes use credit-based insurance scores, which are like credit scores, to help predict whether you’ll file claims. Utility companies can also check your credit and a lower score could lead to larger deposits to obtain their service.

Myth: How much money you make affects your credit score.

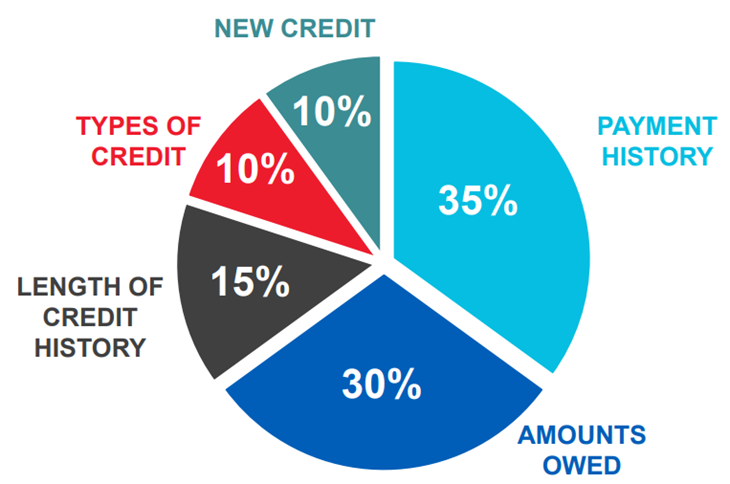

Your income does not directly affect your credit score, nor is it reported to the credit bureaus. Your credit score is determined by five factors:

- Payment History – Payment history is crucial to your credit score because lenders want you to have a history of honoring your financial commitments. Payments made more than 30 days late can have such a negative impact on your credit health.

- Amounts Owed – This is how much debt you carry in total. However, the amount of debt you have is not as significant to your credit score as your credit utilization. Credit utilization is a ratio that represents the amount of credit you’re using divided by total credit available. It’s advised to keep your credit utilization under 30%.

- Length of Your Credit History – A longer credit history shows you have more experience using credit, while a short credit history shows you have less experience.

- Types of Credit – Having a mix of credit account types and paying them off as agreed can help show lenders that you’re responsible.

- New Credit – As part of the application process for loans, the lender may perform a hard inquiry on your credit reports which temporarily lowers your credit score. How often you apply for new credit also plays a role in your score.

Myth: You should avoid credit cards at all costs.

It’s true that irresponsible use of credit cards can lead to debt and negatively impact your credit score. But when used responsibly, your credit cards can help improve your credit score.

How to use credit cards to your advantage:

- Pay your balance off in full each month to avoid paying interest

- Avoid maxing out your credit cards and keep your credit utilization under 30%

- Only spend what you have available to repay

- Pay more than the minimum payment

Myth: Closing your credit card accounts is the best way to improve your score.

Closing your credit card accounts once their balance reaches zero is not the best way to improve your credit score. Considering how your credit score is determined, closing them can possibly hurt your credit score. The most important reason not to close your credit cards – and accounting for nearly 30% of your credit score – is reducing your available credit, which can increase your utilization ratio if you have balances on other cards thus lowering your score. Another important reason why closing your credit cards can negatively impact your credit score is that it can reduce the length of your credit history, which is one of the factors that make up your credit score.

A better strategy to improve your credit score:

- Keep old accounts open even if you don’t use them

- Pay your bills on time (autopay can help)

- Don’t use more than 30% of your available credit card limit

- Avoid opening too many credit accounts in a short time frame – generally speaking, wait at least six months before applying for new credit

- Pay your credit cards in full each cycle

- Pay off any collection accounts

- Frequently review your credit reports for accuracy and keep track of your credit score

Myth: Checking your credit hurts your score.

You can check your credit score at any time without hurting your score if you know where to check. There are two ways to check your credit score: a soft inquiry and a hard inquiry. A soft inquiry does not affect your score. Soft inquiries occur when a person or company checks your credit as part of a background check, or when you check your own score. There are several options where you can pull a soft inquiry credit score check:

- Credit Bureaus such as Experian, TransUnion or Equifax

- Online or mail at AnnualCreditReport.com

- Monitoring apps

A hard inquiry generally affects your score 1-10 points and can stay on your credit report for two years. It’s triggered when applying for a loan or credit such as a mortgage, car loan or credit card. The impact on your score diminishes over time. Multiple hard inquiries in a short period can have a significant impact on your score.

Myth: You can’t get access to credit without an established credit history.

While having a credit history can make it easier to get approved for credit, there are several ways for people with no credit history to start building credit.

Take out a credit builder loan. This type of loan allows you to build credit while growing your savings. The CommunityAmerica ScoreMore Loan1 is a great option to build your credit. The money you borrow is placed in an account that you can’t access until you’ve paid off the loan. We’ll report your on-time monthly payments to the credit bureaus. After your final payment, the savings account is unlocked, and the money is yours.

Become an authorized user. Being added as an authorized user on someone else's credit can help you build credit. You’ll benefit from their good credit habits but make sure they have good credit habits first.

Report your utilities or rent. Some rent and utility reporting services allow these payments to be reported to the credit bureaus. This can be a way to build credit history without getting a loan or a credit card.

Meet with a Financial Well-Being Coach. CommunityAmerica’s Financial Well-Being Coaches offer free expert guidance on budgeting, improving your credit score and managing debt. Start taking control of your credit with a Well-Being Coach to help you achieve financial peace of mind.